QCM CEO Annual Letter 2025

DECEMBER 2025

Aref Karim

Annual CEO Letter

Year Ended 31st December 2025

Dear Investor

The year 2025 was characterised by a series of evolving market conditions rather than a singular prevailing narrative. Shifts in policy expectations, unexpected political developments, and increased fragility in previously reliable correlations posed challenges for investors. Within this context, NexusOne | DivX, launched in January, achieved a full-year return of +7.74%. Realised volatility remained consistent with our 12% target, and the strategy experienced a maximum monthly peak-to-trough drawdown of –6.73%, well within our limits. Additionally, daily correlations were low: –0.02 to the S&P500, and –0.29 to trend strategies as measured by the proprietary QCM EMA Trend index.

Annual Compound Return: +7.74%

Annualised Volatility: +12.37%

Worst Monthly Peak to Trough Drawdown: -6.73%

Daily Correlation with S%P500 Index: -0.02

Daily Correlation with Trend Strategies (ECM EMA Trend Index): -0.29

In its first full year of trading, our focus was on validation. It was as much on how the NexusOne | DivX strategy behaved as on what it returned. On that measure, we are encouraged: the portfolio handled episodes such as the April risk-off shock broadly as designed, containing drawdowns, generating significant crisis alpha in the month and recovering steadily. This was a period when many conventional strategies struggled.

The Year in Markets | Shifting Regimes

The year began with markets still digesting the cumulative impact of the post-pandemic tightening cycle. In the first quarter, investors oscillated between hopes of a benign soft landing and fears that inflation might prove more persistent. Equity indices moved higher, but often on narrow leadership; rates markets swung around each central bank meeting; FX was driven by relative growth and policy surprises.

The April episode provided the first real stress test of the year. A combination of macro and geopolitical concerns triggered a classic “risk-off” move in global equities, a sharp adjustment in bond yields, and a brief flight to quality in selected currencies and commodities. While this was not a full-blown crisis, it was enough to expose hidden concentrations in many portfolios and to remind investors how quickly liquidity can dry up in certain segments.

Through the middle of the year, markets cycled between optimism and caution. Dispersion increased: some equity markets and sectors marched to new highs while others treaded water; yield curves twisted and re-steepened; commodity markets saw very different paths between energy, metals and agriculture.

By the fourth quarter, much of the focus had shifted to the path of policy in 2026, the durability of disinflation, and the behaviour of equity–bond correlations in a world that no longer resembles the pre-2020 “great moderation”. See our recent December Insights feature: The Great Correlation Inversion for more on this.

By year-end, markets were already debating the timing and pace of potential policy easing in 2026, against a backdrop of uneven disinflation and ongoing geopolitical noise. This environment of no single dominant macro theme, but plenty of local trends, reversals and cross-asset dispersion – is exactly what NexusOne | DivX was built for.

Strategy | Behaviour vs Design

NexusOne | DivX is a systematic macro strategy that trades a broad universe of liquid futures across equities, fixed income, FX and commodities. The architecture combines macro thinking with complementary momentum and mean-reversion techniques, modulated by dynamic risk and position sizing.

During 2025, and particularly in the latter part of the year, we rolled out a planned enhanced diversification layer within the existing futures universe. This creates additional internal return pathways across markets, further smoothing how risk is distributed through changing conditions, without altering the overall volatility target or risk budget.

The goal throughout is straightforward: to pursue uncorrelated absolute returns that are robust across regimes, with disciplined control of volatility and drawdowns.

Attribution | Where Returns Came From

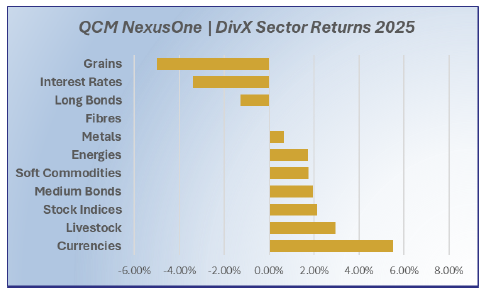

At a high level, 2025’s result was well diversified as per the strategy design, with several parts of the book contributing to the gain. Both Financial and Commodity asset classes were profitable.

The strongest tailwind came from Currencies, where the strategy was able to adapt to shifting policy and risk sentiment and capture a series of medium-sized moves across the year. Livestock, soft commodities, energies and metals also added positively, reflecting a broad mix of commodity-related opportunities rather than a single theme.

Equity index futures delivered a solid positive contribution in a year when global equities were generally strong, but they did not dominate the portfolio. Position-sizing and diversification kept equity risk at a measured level, consistent with our objective of being a genuine macro diversifier rather than an equity proxy.

On the negative side, Grains and short-term Interest Rate futures were the main detractors, with long bonds a smaller drag. These losses came less from one-off shocks than from choppy, stop–start moves as markets repeatedly repriced the path of inflation and policy. Where conditions became disorderly, position-sizing and risk limits helped contain the damage, and risk was redeployed into clearer opportunities elsewhere.

The pattern across the year is visible in the monthly returns: April and October were the strongest months, driven by a broad mix of FX, equity, bond and commodity positions. April, in particular, showed the strategy’s ability to provide crisis alpha during a sharp risk-off episode, while October demonstrated how the same framework can participate in more benign, trend-driven environments. Overall, no single sector or month determined the outcome – which is exactly how NexusOne | DivX is designed to operate.

Risk Management | Liquidity and Adaptability

From the outset, we have treated risk management as a design feature in the strategy, not an afterthought. We target a stable level of portfolio volatility and scale positions accordingly, adjusting as market volatility itself evolves. We continuously monitor the contribution of each sector and trading component to overall risk and to potential stress scenarios. When risk concentrations emerge – particularly in more volatile sectors such as FX or commodities – the system is designed to rebalance and, where appropriate, to reduce exposure.

Crucially, we express all positions through liquid, exchange-traded futures. This allows us to adapt the portfolio quickly as our models update their views. When trends exhaust themselves or when sudden regime shifts occur, we can re-align the book without being constrained by illiquidity or complex structuring.

Our aim is not to eliminate volatility – that would also eliminate returns – but to shape it: to avoid unpleasant, persistent drawdowns, to limit tail risks where we can, and to give investors a smoother path of compounding over time.

The Business | Rebuilding Process

Despite the challenges QCM faced during the previous low-volatility disinflationary cycle of low to negative rates and its business impact of weak performance and capital redemptions, we as a team have approached this new chapter with renewed purpose and determination. By opting for a deliberate and strategic approach to rebuilding, and introducing our next-generation flagship, NexusOne | DivX, we are establishing robust foundations for future growth and sustainability. Each progression is thoughtfully planned and consistently aligned with our overarching long-term objectives.

In 2025 we focused on three priorities:

Delivering a clean first year of performance for NexusOne | DivX that is consistent with its design objectives. We tried to achieve this in one of the toughest years in the markets.

Continuing to strengthen and enhance our infrastructure, with a focus on research and innovation, risk analytics, and operational procedures, while strategically integrating artificial intelligence where appropriate to reduce redundancies and improve operational efficiency.

Engaging with investors – family offices, institutions and other QEPs – who value diversification and are prepared to look beyond headline assets under management.

As part of this effort, we have also begun publishing a series of short monthly “Insights” articles on a broad array of investment and risk topics – including regime shifts, correlation behaviour and portfolio construction. These pieces are intended to give investors a clearer window into how we think about markets and risk, without disclosing proprietary details of the models themselves.

We see this as a rebuilding journey. The current scale allows us to remain nimble and fully aligned with our investors. As we grow, we will remain disciplined on capacity and on staying true to the strategy’s core edge: intelligent diversification, not asset gathering.

The Year Ahead | Looking to 2026

We do not pretend to know exactly how 2026 will unfold; markets rarely oblige one’s forecasts. What we can say is that the opportunity set for a systematic, diversified macro strategy looks compelling.

Policy and rates: Central banks remain in a delicate balance between supporting growth and guarding against renewed inflation. Markets are already focused on the timing and speed of potential policy easing in 2026, and this uncertainty is fertile ground for trends, reversals and cross-country divergences in both rates and FX.

Equity–bond dynamics: The long-standing negative correlation between stocks and bonds is less reliable than it once was. Periods where they move together challenge traditional balanced portfolios but can create opportunities for a strategy that trades both sides actively.

Cross-asset dispersion: Within equities, across curves and within commodities, we expect dispersion to remain high. For a strategy that trades many markets systematically and in multiple layers of diversification, dispersion is attractive raw material.

Geopolitics and energy: Late 2025 also underlined how quickly geopolitical tensions can translate into supply concerns, particularly in energy-producing regions such as Venezuela and its surrounding waters. Such episodes can trigger abrupt shifts in risk premia and correlations across energy, EM and related markets – environments where a diversified, liquid futures portfolio can adapt rather than rely on a single hedge.

NexusOne | DivX is built to adapt across regimes rather than commit to a single view. It is always in the market, but not always in the same way. We will continue to refine and extend the strategy.

In Closing | Conclusion

To our existing investors, thank you for your trust during this first full year of NexusOne | DivX. To those reviewing us for a prospective allocation, we hope this letter provides a clear view of how we think, how we manage risk, and how the strategy behaved in a genuinely challenging market year.

Our job is simple to state but hard to execute: compounding uncorrelated returns, with controlled risk, over many years. We remain fully focused on that objective.

If you would like to discuss any part of this letter, our performance, or our outlook in more detail, we would be very happy to continue the conversation.

Yours sincerely

Aref Karim

Founder, CEO & CIO